Fee for service: You’re Probably

Doing it Wrong

Imagine this: you’re doing a client’s books and you discover a way to save them $4,000 (let’s say the answer lies in A/R). You notice and you spend about an hour setting up a report that highlights aged debtors over 30 days AND you put in place an auto-mailer that chases down debts effectively. What is this worth? An hour of your time or more? For me it comes down to this: I sell services; never time.Think of it another way, when was the last time a potential client called and said “I want to buy two hours of your time”?

Here’s why you should be reading this:

- You are sick of running the ‘price comparison race’

- You want to increase SMB clients

- You want to increase your price for new clients

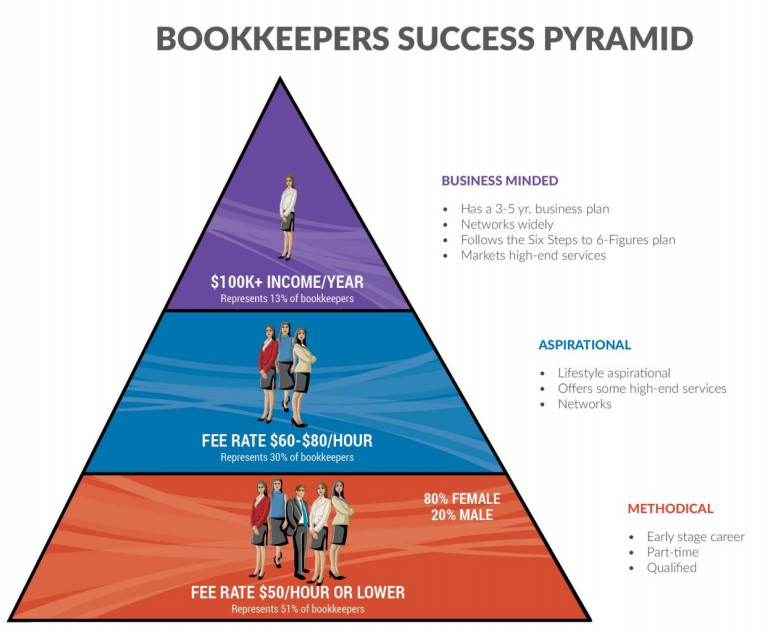

- You want to earn (at least) a six-figure income

Most professionals are too cheap. Most bookkeepers don’t know how to price because most don’t make enough money. Plumbers make more because they solve urgent problems and work in conditions that we would not want to work in. As a profession we are not taught to price and naturally will tend to price as a function of cost. We’re brought up to charge based on hours; it’s a big mistake.

If you were a dog walker or a designer, or a bookkeeper your approach to pricing is probably pretty similar, at least if you’re relatively new to the game. You look at what other people are charging, you think you’re not experienced enough to charge what the high cost providers charge so you go lo-ball. Or you take a look at your costs, figure out what you need to cover them and then add a bit on top for what seems like a reasonable profit and present the final product of these calculations to prospective clients as a daily or hourly rate. It’s a tried and true method, but it’s probably costing you a bucket-load of money and creating schedule feast or famine — periods where you stress through the lean times and run like a lunatic in the busy ones.

There is a better way.

So what’s the answer? Quit all that obsessing about time and focus on value instead. Your clients don’t really care how long it take you to do something; they care about the value it creates for them; the peace of mind for having the compliance stuff done and the benefits of having a dashboard available of how the business is travelling Clock watching isn’t just limiting your income, it’s also downright selfish.

If you want to grow your income you’re going to help customers grow their business. When looked at it like that- from their perspective–it’s clear you’re not selling time. Instead, you’re selling a solution that is going to make an impact for your client and achieve some business objective.

The conversation

The customer wants to maximize your value; this is where our interest are completely aligned. Yet most are terrified to death to talk about money, it is value that determines price not cost. By having an in-depth conversation with prospects about what they’re trying to achieve and really listening to their goals, you can set value-based prices that are higher for you and also deliver more for the client, ideally, offering clients a menu of options to help them reach their objectives.

Getting hard numbers for your clients’ goals is best. Selling hours actually creates a conflict of interest; it puts you and the client on opposite sides of the table. If you’re selling hours, it’s in your best interest to take longer, to bill more hours. But your client is interested in getting solutions that work as promptly as possible, so if you’re asked what your fee is by a prospective client, you need to immediately ask the client a few questions; like “What are your needs?” “What are your biggest concerns?” “What accounting or financial issues are you facing that make you stressed?” Clients care about the value you create for them, so that’s what you should be asking them to pay for.

Of course, this approach doesn’t work for everyone. Hourly rates make sense for someone just starting out, someone with little experience and limited skill. But over time, you begin to outgrow the cost-plus pricing model of charging by the hour. So if you stay with that pricing model, you’ll find it very limiting.

But that’s not the only potential stumbling block to value-based pricing. How do you handle clients that push back against the idea of paying for value? What do you do if your skills aren’t broad enough to meet the client’s fundamental objectives? How can you change your image from a gun for hire to a collaborative partner in solving a client’s problems? And how do you price small jobs and routine maintenance?

Is a six figure income feasible as a professional bookkeeper?

What is certain is that if you lo-ball your rates and get squeezed for extras without billing your six figure income is in doubt. With a six-figure income looking like a pipe dream, it is a more strategic approach that is needed.

For one, you will almost always be competing for the business, sometimes against cut-rate bookkeepers, off-shoring solutions or services that offered inexpensive, do-it-yourself software solutions. Typically a new bookkeeper would try to explain why she was the better choice, but in the end, she may be excused for feeling that if she stuck to her rates, she’d lose out. And at this early stage, she badly needed to build a clientele. So she would often offer discounts, sometimes below her breakeven rate. She wouldn’t be happy about it, but it seemed to be the only way she’d stand a

chance to get the business.

By quoting fees based on conservative estimates, it may work a lot of the time, but it usually means you have to put in more time to finish the jobs. Plus, a lot of clients tended to grind fees down, insisting on extras here and there (scope creep). The result is you might end up making significantly less per hour than the rate you billed.

You need to be aiming for a higher fee structure; to try to increase your rates so it gets a little fairer.

Better still, by quoting a higher rate for added-value work:

The Shopping Cart Approach to Fees

(For the full eBook and our tutorial: A Step-by-Step Guide to Transitioning Your Firm to ValueBilling (including checklist for determining your firm’s suitability for value-billing) log in below or

register for 30-day FREE trial, go to www.bookkeepershub.com.au/register